Saving money might be a breeze now — thanks to platforms like PiggyVest — but it wasn’t always so, at least not in Nigeria. Before banks, automated savings apps, and secure investment websites, many Nigerians had to rely on a different method — Ajo. But what exactly is Ajo?

Ajo is a trust-based informal group savings program where members regularly contribute fixed sums to a common fund. In this system, the group selects one member to receive all the pooled money until the next contribution period, which may vary from daily to weekly or even monthly.

In this article, we’ll explain how Ajo works and explore its history in Nigeria. We’ll also provide a step-by-step guide to doing Ajo online, so you can get started with the savings system using your internet-enabled device.

How does Ajo work?

Ajo is quite popular in many parts of Nigeria, but it might seem somewhat complicated if you’ve never tried it. This method of saving has served many communities for decades and is actually pretty simple to run.

So, how does it work?

Ajo is trust-based, so a program typically begins with members of a close-knit community (like co-workers, neighbours and classmates). These individuals decide how every aspect of the program will work and set all the terms and conditions to which everyone must adhere.

These terms and conditions include the size of the savings group (which can be as few as three individuals or have up to 100 members), the savings amount (say, ₦50,000) and the savings period (daily, weekly or monthly).

They may also set the Ajo termination period — although, traditionally, Ajo savings never end. Instead, members are only allowed to leave after giving their membership to a new individual.

Overall, it’s a sort of genuine democracy in which every member has both equal powers and equal say. However, members of an Ajo group may elect a leader (or groups of leaders, depending on the size of the savings group) to coordinate the affairs of the program by handling fund collection and distribution.

Still, all Ajo savings programs follow the same fundamental rule — they give all of the funds contributed to one member at the end of the savings period. Then they start over and give the funds to another member at the end of the following savings period.

This cycle can continue indefinitely (depending on the terms of the Ajo), but the payout rotation is predetermined by the group or selected at random. However, it’s more common for Ajo groups to practise the former.

To illustrate, let’s consider an Ajo savings group with three friends — Chinedu, Busayo and Idoga. Then let’s assume this group decides that each member will contribute a sum of ₦50,000 to a monthly pool.

Now imagine they also choose to set a termination period of one rotation. And to make things easier, these friends decide that the payout rotation will happen alphabetically — from Busayo to Idoga.

This setup implies that Busayo will receive ₦150,000 at the end of the first month, Chinedu at the end of the second, and Idoga at the end of the third. Afterwards, they’ll cancel the contribution scheme since they set a termination period of one rotation.

What is the history of Ajo in Nigeria?

We’ve already said a lot about Ajo, but it’d be impossible to talk about the savings system in detail without considering its history. So, let’s quickly explore how this informal savings system came into being.

The word “Ajo” itself is the biggest clue to the system’s origins. It is a Yoruba word that translates to “group or organisational savings” in English.

And although there’s very little documentation of the practice’s actual origins, many people believe the system evolved in early Yorubaland as a way for groups to pool their resources to overcome difficult times.

It may have also been a way for members to quickly raise vast sums of money.

Regardless of the actual reason for its origins, the system spread across many communities in Nigeria and beyond since it gave many individuals access to informal savings and credit systems.

And while Ajo might not have the regulations and safety of the traditional banking system, it’s been a part of many African communities (including countries like Liberia and the Democratic Republic of Congo) for many generations.

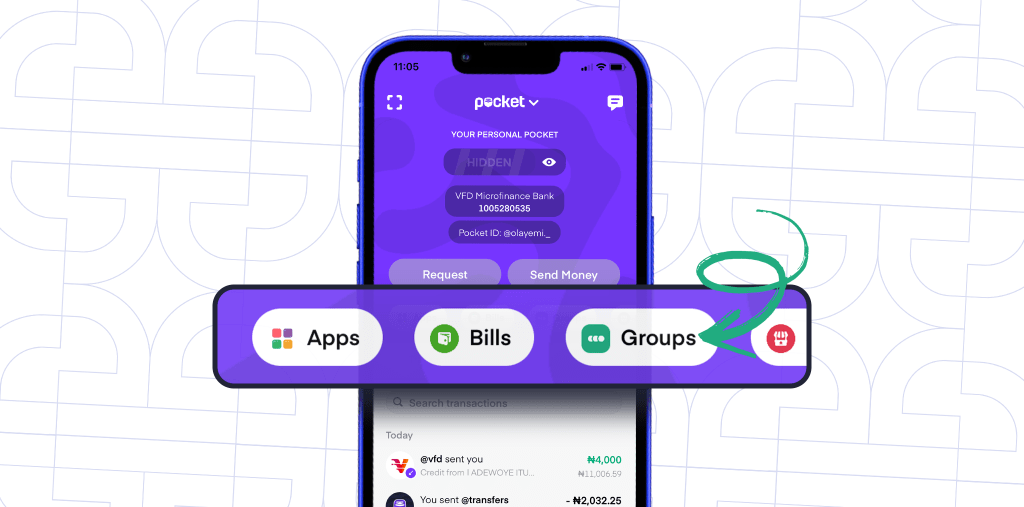

How to do Ajo online using Pocket by PiggyVest

Ajo is pretty straightforward. You can quickly start a regular physical savings group with friends or colleagues. You can also use internet-based alternatives to make the entire process faster, easier and safer. And while there are many options, the best way is to use the Groups feature on PocketApp.

Here’s how to do Ajo online using PocketApp Groups:

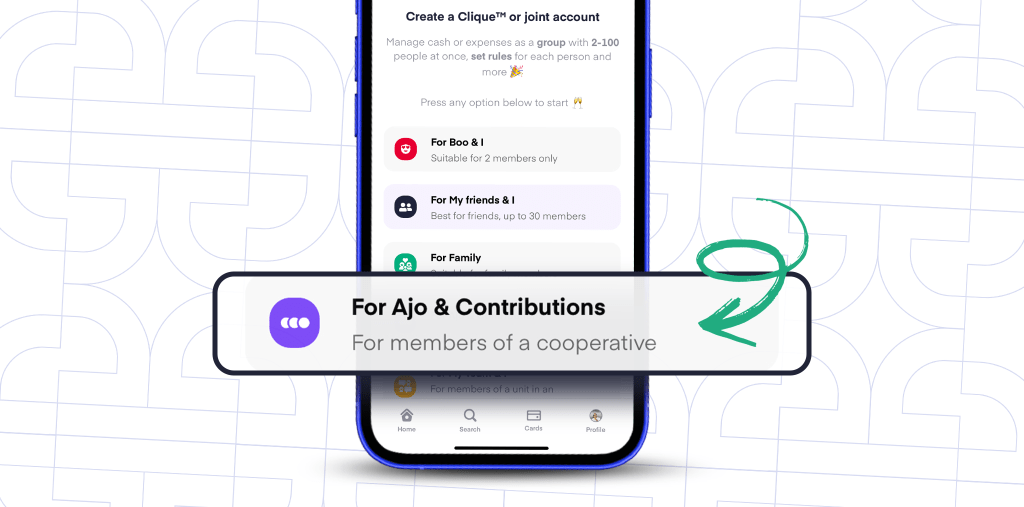

- Select “For Ajo & Contributions” on the Clique™ list and fill in the required details. All you need is the name of the Clique™ and a unique username. For example, you could call your Ajo Clique™ “Family” and set the username to “Hauwa”.

- Tap the “Create Clique™” option. Your new Ajo Group Pocket is now available for use.

- Open your PocketApp and tap the “Groups” option. This action will take you to a screen where you’ll see five joint account (Clique™) options you can explore. You may need to update your app if the feature is unavailable on your PocketApp.

Need a visualizer? The image guides below highlight how easy it is to navigate the Pocket by PiggyVest App when creating your very own online Ajo group!

The PocketApp Ajo Group allows you to do everything you usually would in a regular Ajo system — including managing members and requesting contributions.

There are a few cool features — like added security and the ability to make your Ajo public so anyone can join. And since it’s entirely online, you don’t have to worry about physical collections or tracking down members who haven’t paid yet.

Final thoughts

Saving money might be difficult in Nigeria these days, but saved funds can come in handy in many different situations. And while platforms like PiggyVest offer several fantastic savings options you could choose from, Ajo is also a great alternative.

Fortunately, you can also do Ajo online using PocketApp. It comes with all the benefits of the traditional system and more.